In Donkin & Others v. Federal Commissioner of Taxation [2019] AATA 6746, a recently published decision of the Administrative Appeals Tribunal (AAT), the AAT considered how section 97 of the Income Tax Assessment Act (ITAA) 1936 applied to distributions by the trustee of a family discretionary trust (FDT).

Distributions of income were made to up to five beneficiaries (the Participating Beneficiaries) by resolution of the trustee of the Joshline Family Trust (the JFT), a FDT, for the 2010 to 2013 income years (the Years).

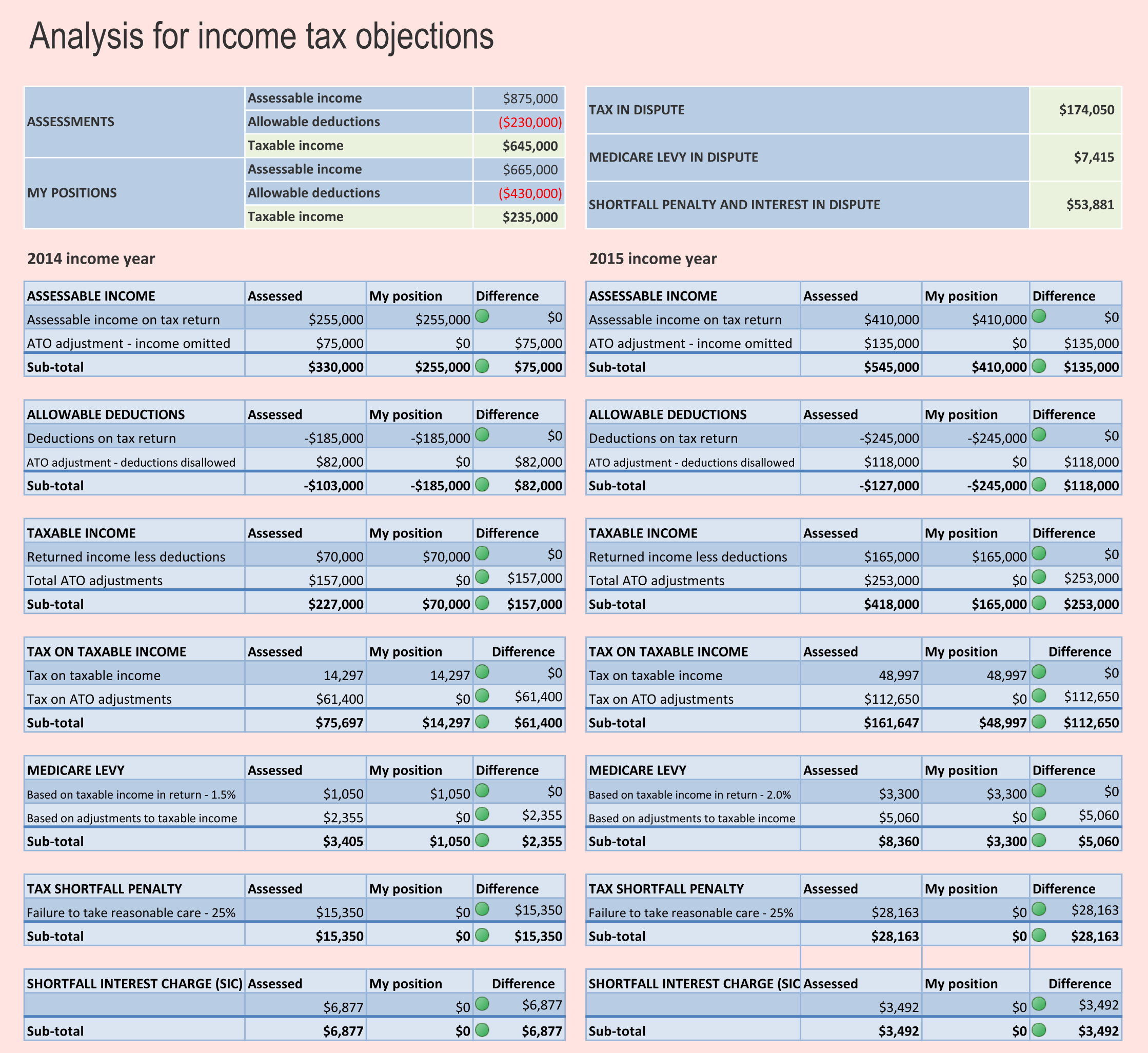

Tax audit – taxable income of the JFT increased

Following an audit of the first Participating Beneficiary, Mr Donkin, and his associated entities the Commissioner of Taxation (Commissioner):

- disallowed deductions to the JFT increasing the taxable income of the JFT for the Years; and so

- increased the taxable income of the JFT.

Before the AAT the Participating Beneficiaries contended that:

- on the increase in the taxable income of the JFT the respective shares of taxable income of the Participating Beneficiaries should remain constant (unaltered); with

- the increase in JFT taxable income taxable to (another) residuary beneficiary Joshline (understood to be a company taxable at no more than 30%).

The Commissioner contended that, based on the High Court authority in Commissioner of Taxation v. Bamford [2010] HCA 10 (Bamford), the proportionate approach should be applied to proportionately increase the taxable income of the Participating Beneficiaries under section 97 from their shares of taxable income on which they were originally assessed.

AAT decides – aligns with Commissioner

The AAT accepted the Commissioner’s contentions and increased the taxable income of:

- the Participating Beneficiaries where section 97 applied; and

- the trustee in respect of Participating Beneficiaries where section 98 applied.

The residuary beneficiary Joshline was not assessed to any of the increase.

Opaque expression of distributable income

The resolutions of the JFT during the Years were odd in that they expressed or specified distributions as amounts of assessable income to which (“trust law”) income (unspecified) was to equate to. The trust deed of the JFT supported this novel approach which was directed to tax planning and, in particular, to certainty of assessable income that each Participating Beneficiary would receive.

These resolutions did not specify distributable income and so obliged a backwards calculation from shares of “assessable income” of the JFT to ascertain the distributable income and the share of it each Participating Beneficiary was entitled to.

How distributable income can be distributed

“Trust law” income, referred to in the legislation as “a share of the income of the trust estate”, considered by the High Court in Bamford to be “distributable income” is, and was described in Bamford as:

income ascertained by the trustee according to appropriate accounting principles and the trust instrument

Bamford at paragraph 45

which can be distributed and which the trustee distributes to beneficiaries and by which the respective shares of assessable income of beneficiaries, and trustees on behalf of other beneficiaries of a trust, is determined under sections 97 and 98 respectively.

If, on a 30 June at the end of an income year (30 June), the trustee has a specified a prescription for the distribution of income of a FDT whether it be:

- an amount (from);

- a set proportion, say expressed in percentage terms; or

- a residue or remaining amount;

of distributable income then that can be accepted understanding that, almost universally, the trustee will not have had the opportunity, by 30 June, to ascertain the distributable income of the FDT to a final figure or amount.

Timing of present entitlement to distributable income

Nevertheless:

- distributions are FDT trustee decisions that need to be made by 30 June if the distributions are to confer present entitlement on beneficiaries in the year of income; and

- beneficiaries must be presently entitled to a share of the distributable income for either of section 97 or section 98 to apply.

Section 99A will apply to a FDT to tax the income to which no beneficiary is presently entitled by 30 June to the trustee at the highest marginal income tax rate. See my post (My Lewski Post) about Lewski v. Commissioner of Taxation [2017] FCAFC 145 where that happened. Lewski was referred to by the AAT in Donkin: Full Federal Court pinpoints year end trust resolutions that fail https://wp.me/p6T4vg-8s

Setting distributable income by 30 June

It follows that to effectively confer present entitlement a trustee decision to distribute trust income under a discretion needs to determine the share of distributable income of each beneficiary by 30 June. That determination of the trustee is confirmed and applied when the trustee prepares accounts for trust purposes in accordance with the terms of the trust deed and, if beneficiaries are entitled to a proportion or a residue of distributable income rather than a fixed amount of distributable income, those entitlements can then be ascertained from distributable income or the remaining distributable income numerically.

Distributable income not set in Donkin

However, in Donkin, the Participating Beneficiaries had entitlements to a proportion of “assessable income” (viz. taxable income or “net income” for the purposes of sub-section 95(1) of the ITAA 1936) (Taxable Income). For instance, under the resolutions Mr. Donkin was entitled to 70.11% of the Taxable Income, not distributable income, of the JFT for the 2013 income year. So in the Commissioner’s contention, as accepted by the AAT, Mr. Donkin was taxable under section 97 on:

- $262,659 being 70.11% of the Taxable Income of the JFT for the 2013 year when an original assessment was raised on Mr. Donkin’s share of trust Taxable Income returned by the trustee of the trust; and then

- $304,137 being 70.11% of the Taxable Income of the JFT for the 2013 year following the amendment of the assessments following the audit.

It can be inferred from and is consistent with the Commissioner’s contention that, on the amendment of Mr Donkin’s 2013 assessment in or around 2015, the distributable income of Mr. Donkin was increased at that later time – the proportion of Taxable Income, 70.11%, did not change.

But how can distributable income of a trust increase after 30 June income year end?

Understanding that the trustee of the JFT determined the distributable income of the JFT and Mr. Donkin’s share of it by 30 June 2013 by mechanisms in the trust deed fixing and thus making Mr. Donkin presently entitled to a share of income confirmable and confirmed when 2013 accounts of the JFT were taken, how can a 2015 amendment to Taxable Income of the JFT alter the 2013 distributable income of the JFT and the present entitlement of Mr. Donkin to it at 30 June 2013?

It seems to me that the AAT has set out good reasons why the Commissioner’s contentions to:

- alter distributable income; and

- increase the present entitlement of each Participating Beneficiary supposedly by the end of the relevant June 30;

should not have been accepted and there should have been no change in distributable income of the Participating Beneficiaries in the Years. In paragraphs 42 and 43 of the AAT’s decision, in a response to different propositions put by the Applicants, the AAT stated:

42. It seems to us that on the Applicants’ construction of the resolutions their alternative submission would be correct. That is to say, the resolutions would be ineffective to confer a present entitlement on the individual beneficiaries because they involved a contingency.

43. They would depend on the occurrence of an event which may or may not happen, in particular, the Respondent disallowing a deduction and including an additional amount in assessable income. It follows that the individual beneficiaries would not be “presently entitled” under ss 97 or 98 of the ITAA36 to a share of the income of the JFT.

Donkin & Others v. Federal Commissioner of Taxation [2019] AATA 6746 paragraphs 42-43

These findings do resonate against the Commissioner’s and the AAT’s construction of the resolutions and the trust deed too.

Construing trust income resolutions applying Bamford

The High Court in Bamford stated:

The opening words of s 97(1) speak of “a beneficiary of a trust estate” who is “presently entitled to a share of the income of the trust estate”. The language of present entitlement is that of the general law of trusts, but adapted to the operation of the 1936 Act upon distinct years of income. The effect of the authorities dealing with the phrase “presently entitled” was considered in Harmer v Federal Commissioner of Taxation where it was accepted that a beneficiary would be so entitled if, and only if,

“(a) the beneficiary has an interest in the income which is both vested in interest and vested in possession; and (b) the beneficiary has a present legal right to demand and receive payment of the income, whether or not the precise entitlement can be ascertained before the end of the relevant year of income and whether or not the trustee has the funds available for immediate payment.”

Bamford at paragraph 37

So in whatever way the trust deed of the trust allows the trustee to ascertain distributable income, the trustee must identify distributable income, or use a method which enables identification of distributable income not subject to contingency, by 30 June to confer present entitlement by 30 June. Without that a beneficiary has no present legal right to demand and receive payment of their share of income by 30 June.

It is that identification of distributable income referred to in Zeta Force Pty Ltd v Commissioner of Taxation (1998) 84 FCR 70 at 74‑75 to which the High Court in Bamford refers where the High Court cites Sundberg J. with approval:

The words ‘income of the trust estate’ in the opening part of s 97(1) refer to distributable income, that is to say income ascertained by the trustee according to appropriate accounting principles and the trust instrument. That the words have this meaning is confirmed by the use elsewhere in Div 6 of the contrasting expression ‘net income of the trust estate’. The beneficiary’s ‘share’ is his share of the distributable income.”

….

“Having identified the share of the distributable income to which the beneficiary is presently entitled, s 97(1) requires one to ascertain ‘that share of the net income of the trust estate’. That share is included in the beneficiary’s assessable income.”

….

from Bamford at paragraph 45

It is respectfully suggested that the later part of Sundberg J.’s findings cited by the High Court:

Once the share of the distributable income to which the beneficiary is presently entitled is worked out, the notion of present entitlement has served its purpose, and the beneficiary is to be taxed on that share (or proportion) of the taxable ncome of the trust estate.

from Bamford at paragraph 45

does not mean that the distributable income of a FDT is to be or can be derived from Taxable Income of the FDT unless that proportion must be quantified or quantifiable, maybe by backwards calculation, by 30 June. For instance, the trustee’s own estimate of Taxable Income on or before 30 June, which could be supported by evidence after the fact, could be a parameter of distributable income which must be fixed if not ascertained by 30 June to achieve present entitlement.

Distributable income at 30 June is then routinely reflected in the accounts of a FDT at 30 June and other evidence which later demonstates what the trustee fixed as distributable income at 30 June.

Why was there no distributable income calculation for each 30 June in Donkin?

The Commissioner too could have worked out the amount of, or the figure for, distributable income of the JFT consistent with resolutions and accounts for the Years and other evidence. including trust tax returns, prepared and lodged later. It is implausible that the trustee of the JFT took into account the 2015 inclusions in Taxable Income in its 2010 to 2013 decisions which the AAT correctly observed was a contingency at the each of the 30 Junes through the Years.

Section 99A should have applied

In my understanding:

- the Participating Beneficiaries in Donkin were not presently entitled in the Years to a proportion of amounts first included in Taxable Income in around 2015 following the Commissioner’s audit and amendment of assessments: and

- section 99A should thus have been applied to these proportions when they became Taxable Income in 2015.

Distributable income – no place for a variable parameter

The AAT appears to have accepted that distributable income can be a variable parameter which can fluctuate after 30 June; the Commissioner and the AAT accepted a distribution method in Donkin based on a set proportion of Taxable Income, a variable parameter, which, in their view, caused distributable income to vary after 30 June when assessments were varied following audit. This sanctioned the use of rubbery numbers for ascertaining shares of distributable income, which the trust deed of the JFT contemplated for opaque tax reasons, without applying section 99A which, in my understanding and based on this analysis, should have applied.

That is disappointing, especially on the urging of the Commissioner, as the AAT decisions may influence future practice and encourage rubbery distributions of distributable income and the use of contorted trust deed provisions that facilitate them.

Income equalisation clauses

Family discretionary trust deeds I have prepared for over thirty years, and deeds drawn by many other preparers, have long based distributions of distributable income on an income equalisation clause. I suggest that an income equalisation clause is, and has always been, a more conventional mechanism for practically dealing with the divergence between distributable income and Taxable Income in section 97 of the ITAA 1936 than the mechanisms contained in the trust deed of the JFT.

An income equalisation clause is a provision in a FDT trust deed which allows the trustee to align the distributable income of a FDT to Taxable Income.

The above analysis is also relevant to how an income equalisation clause using Taxable Income, a parameter that can change after a 30 June year end, should be construed. I addressed this question in My Lewski Post. There I concluded, based on the Full Federal Court’s views of how trust deeds and resolutions are to be construed, that Taxable Income in an income equalisation clause should be construed as Taxable Income based on knowledge of the trustee, informing the trustee’s decision at the time of the distribution, which is confirmed when accounts of the FDT for the relevant income year are taken and the mechanisms from the trust deed for determining distributable income are applied. On that construction Taxable Income is or should be fixed and present entitlement of beneficiaries to shares of distributable income of a FDT at 30 June can thus be attained.