A family discretionary trust (FDT) often has a corporate trustee (TCo) for limited liability and other reasons. With a private company able to access a 30% or lower tax rate on an income distribution received from a FDT, distribution to a private company such as TCo can be a way to access a lower company income rate for a family that does not own or control a private company aside from TCo out of thrift.

But is it a good idea?

Distribution by a FDT to its corporate trustee, TCo, as a “bucket company”, is not necessarily allowable or advisable.

It needs to be understood that FDT deed terms, quality of the FDT deed and FDT set up, including attention to who is a beneficiary of the FDT, vary widely across Australia.

TCo needs to be a beneficiary of the FDT

FDT distributions can only be made to beneficiaries of the FDT. It follows that TCo would need to be entitled in its own right as a beneficiary to a distribution under the terms of the FDT deed. TCo may or may not be a named discretionary beneficiary under the FDT deed.

Many FDT deeds provide for a class of discretionary beneficiary which includes companies owned or controlled by a (some other) beneficiary of the FDT. Sometimes this class is referred to as “eligible corporations” which the FDT deed terms state become beneficiaries of the FDT. These provisions in FDT deeds, if they exist, vary too. Sometimes qualification within a corporate class of discretionary beneficiary turns on someone who qualifies as a beneficiary in the deed:

owning shares in the company; or

being a director of the company;

and it can be just one or the other and not necessarily both.

It can’t be assumed that:

beneficiary qualification in these ways is possible; or

that TCo meets these beneficiary qualifications;

without checking the FDT deed.

Consequences of distributing income to a non-beneficiary

Consequences of a FDT distributing trust income to a person or company who is not a beneficiary under the deed of a FDT can be:

failure of the distribution for legal and tax purposes so that the trustee of the FDT is assessed under section 99A of the Income Tax Assessment Act (ITAA) 1936 with income tax at the highest marginal rate; and/or

treatment of the FDT and distributions from the FDT as a sham by the Australian Taxation Office, other government departments, creditors or others.

Even where TCo may appear to qualify as a beneficiary due to the above, many FDT deeds have overriding exclusionary provisions which exclude persons and companies otherwise specified as beneficiaries from being beneficiaries for various reasons:

Excluded beneficiaries – conflict of interest

Frequently a trustee of a FDT is excluded from being a beneficiary because the trustee, which can exercise the discretion to select discretionary beneficiaries, is in a position of conflict of interest and so TCo, despite qualification as a beneficiary otherwise, is ultimately excluded from being a beneficiary of the FDT. More commonly FDT deeds contain other means which allow a family to control who becomes and acts as a trustee which displaces or should displace inapt conflict of interest considerations as a control redundancy within the deed.

Excluded beneficiaries – stamp duty

But even then a trustee, such as TCo, that may otherwise have qualified as a beneficiary, may still be excluded as a beneficiary by the FDT deed for stamp duty reasons. In New South Wales, in particular, an entitlement to concessional duty under sub-section 54(3) of the Duties Act (NSW) 1997 on a change of trustee of a trust that owns dutiable property can be lost where the a trustee can participate as a beneficiary of the trust.

The consequence of that is a change of trustee of a FDT, say by deed, is treated as a fully ad valorem dutiable transfer of all of the NSW dutiable property of the FDT to the new trustee/s.

Although this limitation of a duty concession varies from other exemptions and concessions applicable to changes of trustee of trusts in states and territories other than NSW, FDT deeds frequently exclude trustees from being beneficiaries out of an abundance of caution that this or a similar stamp duty concession may be lost where the trustee of the FDT is not excluded.

TCo can qualify as a beneficiary – but what then?

If it can be confirmed that TCo does qualify as a beneficiary and is not ultimately excluded as a beneficiary under the trust deed of a FDT, distribution to TCo, rather than another discrete company is still not necessarily a good idea.

Managing TCo’s asset mix

Should TCo receive income from a FDT, and so come to have assets in its own right, TCo will need to manage its assets to ensure that property it holds in its own right and property TCo holds for the FDT are not mixed. A trustee of a trust has a fiduciary duty not to mix trust property with property held not on that trust. This trustee duty is often explicitly set out in FDT deeds.

In terms of title, property distributed to TCo in its own right will be indistinguishable so, without careful accounting and administration of TCo’s activities to ensure trust property isn’t mixed with non-trust property, there is the prospect that a family in control of a FDT may lose track of in which capacity the TCo is owning property and doing things. It will often fall to the accountant of the FDT to sort this out unless the FDT has a very capable and aware functionary administering the FDT for the trustee.

Serious tax risk of losing track of how TCo owns what

Tax risks of unpaid present entitlements (UPE) of TCo in its own right are also high following the recent Draft Taxation Determination TD 2022/D1 Income tax: Division 7A: when will an unpaid present entitlement or amount held on sub-trust become the provision of ‘financial accommodation’? – see our blog post – Draft ATO reimbursement agreement suite out in the wake of Guardian AIT https://wp.me/p6T4vg-q6. Under that draft determination a UPE of a FDT to a private company not detected and promptly repaid (has TCo repaid TCo?) or dealt with under a section 109N of the ITAA 1936 loan agreement, by the time the tax return of the company beneficiary for the income year in which the UPE arises is due, will likely precipitate a deemed and unfrankable dividend to the FDT.

Understanding a company can’t enter into a legally enforceable agreement with itself how could TCo even comply with section 109N as a way to avoid a deemed dividend?

Is distributing to TCo worth it?

Despite the above distribution by FDTs to their corporate trustee as a bucket company is commonplace but done without a keen appreciation of the risks of doing so. I don’t encourage FDTs to distribute to their own trustee even when I am familiar with the trust deed of the FDT. I appreciate there is a cost saving but the costs of running a separate “bucket company”, including the setup and annual ASIC fees and accounting costs, are or should be relatively low so be wary that multi-purposing of TCo can be a false economy for many families with FDTs when the above is taken into account.

Duty on transfer to a discretionary testamentary trust beneficiary

According to Revenue NSW section 63 of the Duties Act (NSW) 1997 does not extend concessional relief to the transfer of dutiable property by a testamentary trust (TT) trustee to a beneficiary.

Concessional duty of $50 applies to:

(a) a transfer of dutiable property by the legal personal representative of a deceased person to a beneficiary, being–

(i) a transfer made under and in conformity with the trusts contained in the will of the deceased person or arising on an intestacy, or …

under sub-paragraph 63(1)(a)(i) of the Duties Act (NSW) 1007

Accepting that a TT trustee is a LPR of a deceased person, or at least disregarding cases where it is not the case, a transfer of NSW real estate by a TT trustee to a TT beneficiary named in the will of the deceased person (Will) in conformity with a TT in the Will appears to make out the requirement of the concession. But Revenue NSW differs.

In Revenue Ruling DUT 46 – Deceased Estates, Revenue NSW states at paragraph 30:

Testamentary trusts

30. Often a will may establish a trust with a named trustee and beneficiaries, with a gift to the trustee of that trust. A transfer from the legal personal representative to a beneficiary of the testamentary trust will not obtain the benefit of the section 63 concession, however, a transfer to the trustee of the testamentary trust will be liable to duty of $50 under sub-paragraph 63(1)(a)(i).

Revenue Ruling DUT 46 – Deceased Estates, Revenue NSW states at paragraph 30

Denial of concession explained?

There is no explanation in DUT 46 as to:

why a transfer to a beneficiary seemingly in conformity with the section 63 concession doesn’t attract the concession; or

how sub-paragraph 63(1)(a)(i) may apply where a beneficiary of a TT has an absolute or indefeasible interest in dutiable property under the TT in the Will.

Scope of statutory exemptions (concessions)

An adage and exhortation about stamp duty, statutory exemptions to duty and those who seek to rely on an exemption is:

find an exemption and get within it

could be trite.

A corollary of no lesser importance is that where a situation doesn’t meet all requirements of an exemption there will be no exemption.

Figuring out what Revenue NSW mean

I understand Revenue NSW to be saying that not all requirements of the formulation:

in conformity with the trusts contained in the will of the deceased person

are met in the case of transfer of dutiable property by a LPR to a TT beneficiary.

Some indication of what Revenue NSW means is at paragraph 7 of DUT 046 which states:

7. The transfer must be made both under and in conformity with the trusts of the will or arising on intestacy. It is not sufficient that the transfer not be inconsistent with those trusts.

with Sanders v Chief Commissioner of State Revenue [2003] NSWADTAP 22 cited in support.

Paragraph 7 hints at the problem an LPR or a TT trustee of a discretionary TT in a Will may have with the section 63 concession. A transfer to a specific discretionary beneficiary in a class of beneficiaries under a discretionary TT is not a stipulation of the testator contained in the Will. The transfer occurs instead because someone other than the testator has been given a power beyond the Will to decide who among the class of TT beneficiaries is to receive the dutiable property.

That exercise of discretion by a living person is extraneous to the Will but is authorised by the Will. Yet, because a discretionary TT beneficiary doesn’t take the dutiable property by direction of the testator and the Will, Revenue NSW seem to say that the transfer is not in conformity with the trusts contained in the Will. That is an undeniably strict interpretation of section 63 bearing in mind that a transfer to an identifiable discretionary beneficiary of a TT to give effect to a valid gift to the beneficiary in the Will is entirely within, anticipated by and “in conformity with” the wishes of a testator expressed in his or her Will.

To describe a transfer made in pursuance of a Will-reposed discretion to gift property among a class of named discretionary beneficiaries as a mere consistency with the Will is somehow inadequate.

Testamentary trust planning

An ongoing discretionary TT included in a Will by a testator may not necessarily be of use to or in the interests of TT beneficiaries who are to take the testator’s property. So a collapsible TT can be desirable and useful to a testator’s survivors instead. Broadly a collapsible TT is where a LPR, TT trustee or appointor is given ability under a Will to collapse a discretionary TT and take the TT property as if the Will had made a gift of the property bypassing holding the property on the TT.

Based on the above such a gift on collapse of a discretionary TT to a named beneficiary is or should be wholly in conformity with a stated gift in the Will and so should attract concessional duty under sub-paragraph 63(1)(a)(i). It follows that a collapsible TT can lead to a duty saving where:

the TT is over property including dutiable property;

the TT is collapsed, bypassed and doesn’t take effect as a TT; and

the dutiable property that was to be held on the TT is instead transferred to the named beneficiary expressly under the terms of the Will and the sub-paragraph 63(1)(a)(i) exemption can thus be made out.

Containment

So to achieve a stamp duty exemption in conformity with the trusts contained in the Will under the Revenue NSW regime no actions extraneous to the Will, such as the exercise of a Will-based discretion to distribute dutiable property to a TT beneficiary, are “within” the concession. That is: the gift pathway of the dutiable property from testator to beneficiary needs to be wholly contained in the Will.

Perpetuities

There is a curious comparison between the approach of Revenue NSW to duty on transfer by a LPR to a discretionary TT beneficiary and the approach of the Federal Court to the rule against perpetuities.

In an earlier blog How perpetuities law limits can impact trust distributions to other trusts I considered the “wait and see” rule as it applies to the perpetuities following the Federal Court decision in Federal Court in Nemesis Australia Pty Ltd v Commissioner of Taxation [2005] FCA 1273. What would the outcome in that case have been if such a narrow or strict approach to the “wait and see” rule, which is effectively an exemption from the common law rule against perpetuities now codified by statute in most states (the Perpetuities Rule), been taken?

All jurisdictions except South Australia have retained the Perpetuities Rule.

Uneasiness

I am uneasy about the Nemesis Australia decision as the last words in my blog suggest. If Nemesis Australia is later found by a court to be incorrectly decided then the consequences will be severe for trusts impacted: where the Perpetuities Rule applies to a trust, the trust is void and treated as if it was never valid. This harshness was the reason for the introduction of “wait and see” rule, under which dispositions of property under a trust, that would otherwise be void under the Perpetuities Rule, are not void from the outset and the parties can “wait and see” whether the disposition of property under the trust will vest within the applicable perpetuity period. Only where the property does not so vest is the trust then invalidated by the Perpetuities Rule.

Policy to prevent remoteness of vesting

The policy of the Perpetuities Rule (the Policy) is:

to prohibit lengthy remoteness of vesting of property interests in private hands and indestructible private trusts;

to limit property owners’ capacity to restrict free alienation of property ; and

to limit the control of property by trust founders or testators to a reasonable period.

The Perpetuities Rule applies to private trusts aside from charitable trusts and superannuation funds to achieve this Policy.

Significance of a trust discretion

The Nemesis Australia decision turned on the significance of an exercise of a discretion: it was found that the “wait and see” rule could be applied because the trustee of Trust B had a discretion to bring forward the vesting day and the parties could then “wait and see” whether the vesting day of Trust B will be brought forward by exercise of discretion to the earlier vesting date of Trust A. Should that happen property from Trust A, received into Trust B as a distribution from Trust A, would not vest outside of the Perpetuities Rule perpetuity period for property vested in Trust A. (See my blog How perpetuities law limits can impact trust distributions to other trusts )

Disparity of approach to statutory exemptions

There is a disparity between how the “wait and see” rule was interpreted in Nemesis Australia where a discretion, whose exercise is not dictated by the terms of a trust, was acceptable to invoke the “wait and see” rule and Revenue NSW’s rejection of exercise of a Will-based discretion not dictated by a Will as not being in conformity with the trusts in a Will for section 63 of the Duties Act 1997 purposes.

There are a number of principles of statutory interpretation that can be applied to exemptions which were not considered in Nemesis Australia. These principles do not support a construction of the “wait and see” rule that saves a trust from being void under the Perpetuities Rule where the parties wait to see if a trust terms-based discretion will be exercised to bring forward the vesting date of the trust:

an interpretation of a statute which will permit a person to take advantage of his or her own wrong is to be resisted (Resistance); and

an interpretation of a statute that promotes the purpose of a statute is to be preferred to a literal construction (Preference).

Resistance

An instance of a Resistance given in Pearce & Geddes “Statutory Interpretation” 7th ed. is in Holden v. Nuttall (1945) VLR 171 where, on an application for possession of leased premises, a court was required by statute to take into account whether an order for possession would cause the lessee “hardship”. Evidence showed that the lessee had acted in a manner contrived by the lessee to enable him to take the benefit of the hardship exception. Herring CJ found that the meaning of “hardship” should be limited so that no injustice would be brought about by allowing a person to benefit from his or her own wrong.

This is comparable to where a trust is established with say a last vesting date of 160 years which is well beyond perpetuity periods allowed under Perpetuity Rules. (See also the similar hypothetical raised by the Respondent referred to in paragraph 43 in the judgement in Nemesis Australia.) This differs much from a case of say, a trust where when property may vest turns on a genuine and unplanned contingency or contingencies that may or may not occur within the perpetuity period, such as how long a beneficiary of a trust may live for, which is the type of contingency the “wait and see” rule ordinarily contemplates.

Still trust terms may allow a trustee, or some other person; a discretion to bring forward the vesting day as in Nemesis Australia, or even in the absence of a term allowing the bring forward of the vesting date of the trust, state law may allow a trustee to apply to a state court for a vesting order prior to expiry of the applicable perpetuity period. If Nemesis Australia is correctly decided the parties to the trust may then “wait and see” whether a vesting order is applied for and vesting happens within the perpetuity period of a trust flagrantly in breach of the Perpetuity Rule and the Purpose and, in the meantime, the trust would be valid.

But a 160 year last vesting date for a trust may be a wrong, such as considered in Holden v. Nuttall, by the founder of a trust. That is a wrong that is contrary to the Policy when considered in the context of the Policy. Shouldn’t a trust established on the premise of that wrong, if it is a wrong, be considered:

contrived to take advantage of the “wait and see” rule?; and

beyond what is meant as a “wait and see” under the “wait and see” rule?;

and denied “wait and see” exemption from the Perpetuities Rule?

Preference

The construction of the “wait and see” rule in Nemesis Australia is literal. The Preference, as Pearce & Geddes explain, is that an interpretation of a statutory provision under section 15AA of the Acts Interpretation Act (C’th) 1901 and comparable state and territory legislation should promote a construction of a statute based on the purpose of a statute as preferable to a literal construction.

Pearce & Geddes also refer to the explanation of Dawson J. in Mills v. Meeking (1990) HCA 6 at para. 19 as follows:

19. However, the literal rule of construction, whatever the qualifications with which it is expressed, must give way to a statutory injunction to prefer a construction which would promote the purpose of an Act to one which would not, especially where that purpose is set out in the Act. Section 35 of the Interpretation of Legislation Act must, I think, mean that the purposes stated in Pt 5 of the Road Safety Act are to be taken into account in construing the provisions of that Part, not only where those provisions on their face offer more than one construction, but also in determining whether more than one construction is open. The requirement that a court look to the purpose or object of the Act is thus more than an instruction to adopt the traditional mischief or purpose rule in preference to the literal rule of construction. The mischief or purpose rule required an ambiguity or inconsistency before a court could have regard to purpose: Miller v. The Commonwealth (1904) 1 CLR 668 at p 674; Wacal Developments Pty. Ltd. v. Realty Developments Pty. Ltd. (1978) 140 CLR 503 at p 513. The approach required by s.35 needs no ambiguity or inconsistency; it allows a court to consider the purposes of an Act in determining whether there is more than one possible construction. Reference to the purposes may reveal that the draftsman has inadvertently overlooked something which he would have dealt with had his attention been drawn to it and if it is possible as a matter of construction to repair the defect, then this must be done. However, if the literal meaning of a provision is to be modified by reference to the purposes of the Act, the modification must be precisely identifiable as that which is necessary to effectuate those purposes and it must be consistent with the wording otherwise adopted by the draftsman. Section 35 requires a court to construe an Act, not to rewrite it, in the light of its purposes.

Dawson J. in Mills v. Meeking (1990) HCA 6 at para. 19

The purpose of the Perpetuities Rule is the Policy. The Policy is defeated where a contingency that a trustee could apply for a vesting order prior to the expiry of the perpetuity period applicable to the trust prevents the Perpetuities Rule from taking effect in an abundance of cases. The Respondent’s submission referred to in paragraph 43 in the Nemesis Australia judgement cogently establishes why the Policy fails where the “wait and see” rule is applied literally but the Federal Court in the Nemesis Australia seemed to gives minimal credence or importance to the Policy as the legislative intent of the Perpetuities Rule.

Conclusion

All requirements to make use of a statutory exemption from a law need to be met. Occasionally exemptions, including exemptions which are not clearly expressed, will be construed strictly perhaps to unanticipated standards. Equivocally drafted statutory exemptions can lead to unexpected outcomes so, where much turns on whether or not an exemption is available, caution should be exercised and a conservative approach taken.

Hopefully Revenue NSW’s view in paragraph 30 of Revenue Ruling DUT 46 on duty on transfers of dutiable property to a beneficiary of a testamentary trust will eventually be tested and explained in a reported court decision.

With regard to perpetuities, the Perpetuities Rule and the “wait and see” rule I suggest that appropriate fail safes should be included in discretionary trust deeds so that the Perpetuities Rule can be complied with and the trust will remain valid, just in case Nemesis Australia doesn’t persist as the accepted Australian understanding of how the “wait and see” rule applies on some basis I have or haven’t anticipated.

Clip Royalty Free Stock Country Passport Stamps Clipart – Australia @seekpng.com

Laws reflect perspective. When the imposition of laws, especially taxes, turns on whether the taxpayer is a local (resident) or foreign (non-resident) then laws will be designed with elusion in mind so someone cannot elude being treated as:

local if the burden and focus of the law (such as a tax) falls on locals; and

foreign if the burden and focus of the law falls on foreigners.

Income tax – focus on locals

The Income Tax Assessment Act (C’th) (ITAA) 1936 overall might be considered to be in the former case in Australia. Although Australian non-resident income tax rates can be higher than resident rates, generally a wider range of activity of residents is taxable in Australia, and residents are subject to income tax on their worldwide income. Income tax collection under the ITAA 1936 and 1997 is mainly focussed on collecting income tax from residents. Certainly Australian locals can be income taxed with fewer international constraints.

Thus who is a “resident” or “resident of Australia” in the definition of these terms in sub-section 6(1) of the ITAA 1936 includes, among others: an Australian citizen whose domicile, by virtue of that citizenship, is in Australia unless the Commissioner of Taxation is satisfied the person’s permanent place of abode is outside of Australia. This definition part imposes a satisfaction hurdle without which an Australian citizen, with a domicile in Australia, will be an income tax resident with broad exposure to income tax under the ITAA 1936 and 1997.

Foreign acquisitions and takeovers – focus on foreigners

In contrast the burdens imposed by the Foreign Acquisitions and Takeovers Act (C’th) 1975 (FATA) in Australia are on foreigners and is so, along with the state and territory foreign person surcharges mentioned below, an example of the latter case in Australia. The FATA is concerned with the acquisition, monitoring and control of Australian real estate and other Australian-based investment interests by foreigners. The FATA obliges notification to the Foreign Investment Review Board (FIRB) of proposed acquisitions of specified types which can be approved or rejected by the Australian Treasurer on the recommendation of the FIRB.

Vacancy fee

A vacancy tax on foreigners commenced under the FATA as a measure to improve housing affordability for Australian locals in 2017. The vacancy fee is contained in Part 6A of the FATA under which a foreign person who owns a residential dwelling in Australia is charged an annual vacancy fee where the dwelling is not residentially occupied or rented out for more than 183 days in yearly periods which measure from the date of acquisition of ownership by the foreigner. The vacancy fee under Part 6A is imposed as a tax by section 5 of the Foreign Acquisitions and Takeovers Fees Imposition Act (C’th) 2015.

Vacancy fee rates

Vacancy fee rates are tethered to the FIRB fees (also imposed as taxes under the same section 5) applicable to a foreign person making an application to acquire the residential land. which is ad valorem based on the value of the real estate on acquisition. Here is an extract from a table with the ad valorem fees:

Acquiring an interest in residential land where the price of the acquisition is…

“foreign person” means: (a) an individual not ordinarily resident in Australia; or (b) a corporation in which an individual not ordinarily resident in Australia, a foreign corporation or a foreign government holds a substantial interest; or (c) a corporation in which 2 or more persons, each of whom is an individual not ordinarily resident in Australia, a foreign corporation or a foreign government, hold an aggregate substantial interest; or (d) the trustee of a trust in which an individual not ordinarily resident in Australia, a foreign corporation or a foreign government holds a substantial interest; or (e) the trustee of a trust in which 2 or more persons, each of whom is an individual not ordinarily resident in Australia, a foreign corporation or a foreign government, hold an aggregate substantial interest; or (f) a foreign government; or (g) any other person, or any other person that meets the conditions, prescribed by the regulations.

section 4 of the FATA

It follows that any person, including an Australian citizen, can be a foreign person caught by these provisions however, under a convoluted exemption arrangement, Australian citizens who are not ordinarily resident in Australia are relieved from the vacancy fee.

Relief for non-resident Australian citizens

I understand that the relief works in this way:

Section 28 of the Foreign Acquisitions and Takeovers Regulation 2015 [Select Legislative Instrument No. 217, 2015] (FATR 2015) prescribes every section of the FATA, aside from the definition of foreign person in section 4 itself and other provisions to which that definition relates to, as excluded provisions. (Bold emphasis added by me.)

Section 28 also carries a note which provides:

The effect of this Division is that acquisitions of interests of a kind mentioned in this Division are not significant actions, notifiable actions or notifiable national security actions, but are taken into account for the purposes of the definition of foreign person in section 4 of the Act.

Note to section 28 of the FTAR 2015

and

paragraph 35(1)(a) of FATR 2015 provides:

Acquisitions of any land by persons with a close connection to Australia

(1) The excluded provisions do not apply in relation to an acquisition of an interest in Australian land by any of the following persons:

(a) an Australian citizen not ordinarily resident in Australia;

…

paragraph 35(1)(a) of FATR 2015

There does not appear to be any further “close connection”, as referred to in the heading to section 35, required to trigger the exemption beyond being an Australian citizen in the case of paragraph 35(1)(a). That is: a non-resident Australian citizen has, by virtue of being a citizen, a close connection to Australia.

Application of the non-resident Australian citizen exemption to the vacancy fee?

The vacancy fee, though, is a tax imposed on a foreign person when a dwelling, already acquired by the foreign person, is not residentially occupied or rented out for more than 183 days in yearly period as stated above. Could it be that a foreign person, including a non-resident Australian citizen, will still be caught by the vacancy fee because the vacancy fee is concerned with omission to occupy or rent out property for more than 183 days over a yearly period and not with acquisition of the property so paragraph 35(1)(a) relief can’t be attracted?

The answer appears to be in section 115B of the FATA which scopes when vacancy fee liability under Part 6A arises. Section 115B provides:

Scope of this Division–persons and land (1) This Division applies in relation to a person if: (a) the person is a foreign person; and (b) the person acquires an interest in residential land on which one or more dwellings are, or are to be, situated; and (c) either: (i) the acquisition is a notifiable action; or (ii) the acquisition would be a notifiable action were it not for section 49 (actions that are not notifiable actions–exemption certificates). Note: Regulations made for the purposes of section 37 may provide for circumstances in which this Division does not apply in relation to a person or a dwelling….

sub-section 115B(1) of the FATA

It follows that the provisions of “this Division”, which is Division 2 of Part 6A of the FATA and which contains the provision imposing vacancy fee liability, are excluded provisions and so vacancy fee liability on an omission to occupy or rent residential land, where the interest in that residential land was acquired by a non-resident Australian citizen under paragraph 35(1)(a) of FATR 2015, is not attracted by a non-resident Australian citizen purchaser of the residential land. That is so even though a non-resident Australian citizen is a foreign person caught by paragraph 115B(1)(a).

This is a very complicated way to exempt non-resident Australian citizens from treatment as foreigners. Couldn’t section 4 of the FATA just carve out non-resident Australian citizens from being foreign persons to broadly the same effect?

Adding to the confusion is FIRB Guidance Note 31 Who is a foreign person (1 July 2017) which refers to paragraph 15 of the decision in Wright v. Pearce (2007) 157 CLR 485 as guidance on the position with Australian citizens. This reference is actually in error and should be Wight v. Pearce (2007) 157 FLR 485 (not a decision of the High Court of Australia). In any case I can’t see where that reference has anything to say about resident and non-resident Australian citizens having a close connection to Australia, which, unlike being ordinarily resident in Australia which is the matter under consideration at paragraph 15 of the case, is the apparent touchstone of liability when paragraph 35(1)(a) of FATR 2015 is taken into account.

Comparison of the federal vacancy fee with state foreign person surcharge land tax and surcharge purchaser duty

The foreign person surcharges in New South Wales also adopt the “foreign person” formulation in section 4 of the FATA to pinpoint foreigners liable to the surcharges but with modifications including under paragraph 104J(2)(a) of the Duties Act (NSW) 1997:

(a) an Australian citizen is taken to be ordinarily resident in Australia, whether or not the person is ordinarily resident in Australia under that definition,

paragraph 104J(2)(a) of the Duties Act (NSW) 1997

which carves out non-resident Australian citizens from “foreign persons” and thus the complexity of excluded provisions from the FATR 2015, a Commonwealth statutory instrument, do not need to be contended with to find exemption for non-resident Australian citizens from the surcharges.

In making a comparison between the the federal vacancy fee on the one hand with state foreign person surcharge land tax on the other hand it should also be observed that the state foreign person land tax surcharges are generally imposed on foreigners per se, that is: whether the residential land is vacant for a period is immaterial. So omission by a foreign person to occupy or rent out property for more than 183 days generally means liability for both the federal vacancy fee and a state land tax surcharge will be attracted.

Temporary residents

When an individual owner of residential real estate is not an Australian citizen then whether the individual is ordinarily resident in Australia does become a touchstone for tax and surcharge liability as a “foreign person”. Sub-section 5(1) of the FATA provides:

(1) An individual who is not an Australian citizen is ordinarily resident in Australia at a particular time if and only if:

(a) the individual has actually been in Australia during 200 or more days in the period of 12 months immediately preceding that time; and

(b) at that time:

(i) the individual is in Australia and the individual’s continued presence in Australia is not subject to any limitation as to time imposed by law; or

(ii) the individual is not in Australia but, immediately before the individual’s most recent departure from Australia, the individual’s continued presence in Australia was not subject to any limitation as to time imposed by law.

Sub-section 5(1) of the FATA

A temporary resident for tax is someone who is not an Australian citizen or permanent resident who can stay in Australia under an immigration visa which, as a matter of course, will be a visa with a limitation as to the time the holder can stay in Australia.

A temporary resident is taxable for income tax only:

on income derived in Australia; and

on foreign income but only foreign income earned from employment or services performed overseas while a temporary resident.

A temporary resident is not income taxable on capital gains made on assets which are not Taxable Australian Property e.g. real estate.

A temporary resident is a foreign person under the FATA no matter how long the individual is present in Australia until and unless the temporary resident becomes a permanent resident or an Australian citizen due to paragraph 5(1)(b) of the FATA as set out above.

Temporary residents can acquire residential real estate, including established residential premises with conditions, under the FATA and FIRB regime however the vacancy fee and the state and territory foreign person surcharges can apply to their interests in Australian residential land.

Permanent residents

As permanent resident visa holders are not subject to any limitation as to time they can be in Australia imposed by law the requirements in paragraph 5(1)(a) of the FATA are of ongoing concern to them until and unless they become Australian citizens. That is: a permanent resident who has not actually been in Australian for 200 days in the applicable preceding twelve months is taken not to be ordinarily resident in Australia despite their visa.

If such a permanent resident owns Australian real estate but has not been in Australia for the required 200 days in an applicable twelve months then he or she is a foreign person for that year. Then the vacancy fee and the state and territory foreign person surcharges can apply to a permanent resident’s interests in Australian residential land.

Advent of the state foreign person property surcharges

Foreign person surcharges have applied on New South Wales, Victoria, Queensland, Tasmania, Western Australia and Australian Capital Territory property taxes following Commonwealth action to have the Foreign Investment Review Board more closely monitor the acquisition and holding of Australian real estate by foreign interests: see our July 2016 blog post:

(a) a surcharge purchaser duty (currently 8% of the market value of the property) on the acquisition of residential property in NSW (Chapter 2A of the Duties Act (NSW) 1997 [DA]); and

(b) a surcharge land tax (currently 2% of the unimproved value of the land) for residential property in NSW owned as at 31 December each year (section 5A of the Land Tax Act (NSW) 1956).

(Surcharges)

The foreign trusts that aren’t foreign problem

Discretionary trusts with all or predominantly Australian participants and entitled beneficiaries can nevertheless be caught as foreign trusts that must pay the Surcharges. Liability for the Surcharges is based or grounded on sub-section 18(3) of the Foreign Acquisitions and Takeovers Act (C’th) 1975 (FATA): Sub-section 18(3) provides:

For the purposes of this Act, if, under the terms of a trust, a trustee has a power or discretion to distribute the income or property of the trust to one or more beneficiaries, each beneficiary is taken to hold a beneficial interest in the maximum percentage of income or property of the trust that the trustee may distribute to that beneficiary.

sub-section 18(3) of the Foreign Acquisitions and Takeovers Act (C’th) 1975

If the income or property (capital) that could be distributed to a foreign beneficiary of a trust is 20% or more of income in a year or property of the trust, the trust is foreign for FATA and Surcharge purposes. An ameliorating aspect of the Surcharges legislation is that:

Australian citizens who are non-residents of Australia; and

some New Zealand citizens with certain Australian visas;

who are foreign persons under the wide sweep of sub-section 18(3) of the FATA are excluded from being foreign persons for NSW Surcharges purposes: see sub-section 104J(2) of the DA.

The lengthy transition

Even for those not averse to the idea that foreign individual and foreign trust investors should pay higher property dues the implementation of the Surcharges in NSW has been agonising. Even now, in 2020, four years after liabilities for Surcharges were first imposed under the DA and the LTA the State Revenue Legislation Further Amendment Act (NSW) 2020 (“SRLFAA”) is still needed to phase in the Surcharges, and transitional relief from them, as they apply to trusts.

As well as imposing the wide sweep of what the FATA treats as foreign, the SRLFAA:

imposes impugnable trust deed requirements on discretionary trusts (see below); and

extends transitional arrangements that were set to end on earlier dates in versions of Revenue Ruling G010 from Revenue NSW and the State Revenue Legislation Further Amendment Bill (NSW) 2019.

Trust deed requirements on discretionary trusts

Where a trust is a discretionary trust for Surcharge purposes then the SRLFAA requires that the terms of the trust must be amended by 31 December 2020 so:

(a) no potential beneficiary of the trust is or can be a foreign person [the no foreign beneficiary requirement]; and (b) the terms of the trust cannot be amended in a manner so a foreign person could become a beneficiary [the no amendment requirement];

and then only does the discretionary trust, even a discretionary trust that:

has no foreign participants or beneficiaries; and

thus is not foreign after the FATA wide sweep and sub-section 104J(2) of the DA are considered;

(a Local DT) escape treatment as a foreign trust for Surcharge purposes.

Why the no amendment requirement?

The object of the no amendment requirement is to impose the Surcharges based on the contingency or possibility only that a Local DT may come to have a foreign beneficiary in the future. The position of Revenue NSW is understood to be that Revenue NSW does not have the compliance resources to monitor Local DTs for foreign beneficiaries into the future on an ongoing basis.

Although nearly all discretionary trust deeds contain some kind of variation power, a design fault of such resource-saving requirements viz.:

the “irrevocable” requirement of Revenue NSW in paragraph 6 of Revenue Ruling DUT 037 concerning sub-section 54(3) of the DA concerning concessional duty on changes of trustee; and

the no amendment requirement now in the SRLFAA;

is that the variation power in many or most trust deeds of trusts in NSW may not permit modification of the variation power to satisfy either of these requirements.

Changing the scope or amending the terms of a trust amendment power

In Jenkins v. Ellett, Douglas J. of the Queensland Supreme Court stated the relevant law and learning about changing the variation power in a trust deed:

[15] The scope of powers of amendment of a trust deed is discussed in an illuminating fashion in Thomas on Powers (1st ed., 1998) at pp. 585-586, paras 14-31 to 14-32 in these terms:

“In all cases, the scope of the relevant power is determined by the construction of the words in which it is couched, in accordance with the surrounding context and also of such extrinsic evidence (if any) as may be properly admissible. A power of amendment or variation in a trust instrument ought not to be construed in a narrow or unreal way. It will have been created in order to provide flexibility, whether in relation to specific matters or more generally. Such a power ought, therefore, to be construed liberally so as to permit any amendment which is not prohibited by an express direction to the contrary or by some necessary implication, provided always that any such amendment does not derogate from the fundamental purposes for which the power was created ….It does not follow, of course, that the power of amendment itself can be amended in this way. Indeed, it is probably the case that there is an implied (albeit rebuttable) presumption, in the absence of an express direction to that effect, that a power of amendment (like any other kind of power) cannot be used to extend its own scope or amend its own terms. Moreover, a power of amendment is not likely to be held to extend to varying the trust in a way which would destroy its ‘substratum’. The underlying purpose for the furtherance of which the power was initially created or conferred will obviously be paramount.”

Jenkins v. Ellett [2007] QSC 154

In our experience a small minority of trusts in NSW have a variation power which expressly permits extension of its own scope or amendment of its own terms. That kind of extended power can raise its own set of difficulties which explains why these extended variation powers are not especially popular. It follows, as stated, that a substantial number of variations of the terms of discretionary trust deeds which the no amendment requirement imposes are prone, or likely, to be beyond the power conferred by the variation power of the trust and thus ineffective on a trust by trust reckoning.

discretionary trust for Surcharges purposes

In section 1 in the dictionary of the DA a discretionary trust is defined for DA and Surcharges purposes:

“discretionary trust” means a trust under which the vesting of the whole or any part of the capital of the trust estate, or the whole or any part of the income from that capital, or both– (a) is required to be determined by a person either in respect of the identity of the beneficiaries, or the quantum of interest to be taken, or both, or (b) will occur if a discretion conferred under the trust is not exercised, or (c) has occurred but under which the whole or any part of that capital or the whole or any part of that income, or both, will be divested from the person or persons in whom it is vested if a discretion conferred under the trust is exercised.

section 1 of the dictionary of the Duties Act (NSW) 1997

More time to check for unexpected foreign trust treatment

With time extended to 31 December 2020 by the SRLFAA to amend trust deeds so a discretionary trust won’t be treated as a foreign person it is timely during the remainder of 2020 to also check the terms of residential land holding trusts that may not ordinarily be thought of as a discretionary trust.

A trust, including a unit trust, that contains powers in its terms which:

allow for a beneficiary to be selected by someone to take income or capital;

allow for the amount of income or capital a beneficiary is to take to be set by someone;

which can change the income or capital a beneficiary will take if the discretion is not exercised; or

which can divest a beneficiary of an interest in income or capital which they otherwise would take;

that brings the trust within a discretionary trust in section 1 of the dictionary of the DA needs to meet the no foreign beneficiary requirement and the no amendment requirement in the SRLFAA.

Hybrid trusts and other unit trusts

This definition brings in trusts known as hybrid trusts within this construct of discretionary trust. Shortly stated a hybrid trust is a tax aggressive structure where unit or interest holders have standing vested interests in income or capital of the trust but where, usually, the trustee has a supervening power or powers to divest those interests in income, capital or both in favour of other beneficiaries such as family or related companies or trusts controlled by the unit or interest holder with the standing interest.

Other unit trust arrangements can be treated as a DA discretionary trust even where the discretion is historical, redundant and income tax benign. For instance an older style standard unit trust may be set up by way of initial units and the trustee may be given a discretion in the trust deed not to distribute income or capital to initial unitholders once ordinary units in the trust are issued.

This discretion in the terms of a trust is enough for the unit trust to be treated as a discretionary trust so it would be prudent for the terms of the unit trust to be amended to remove the discretion if that can be done:

without resettling the trust; and

less onerously than amending the trust deed to comply with the no foreign beneficiary requirement and the no amendment requirement.

It is sometimes

wrongly assumed that a minute of the current trustee is sufficient to change

the trustee of:

a family

discretionary trust (FDT); or

a self

managed superannuation fund (SMSF) (which must be a trust with a trustee too –

see sub-section 19(2) of the Superannuation

Industry (Superannuation) Act (C’th) 1993 (SIS Act));

and that a change of

trustee will have no serious tax consequences. The second proposition is more

likely to be true, but not always.

FDTs and SMSFs

invariably commence with a deed which contains the terms (the trust terms or

governing rules – TTOGRs) on which the trust commences. That, in itself, is a

reason why I contended in 2009 in Redoing the deed

that an instrument or resolution less than a deed to change the trustee is

prone to be ineffective even where change by less than or other than a deed is

stated to be permitted by the TTOGRs in the trust deed.

Changing trustee

relying on ability to change in the trust deed

It is thus to the

trust deed that one needs to look to find:

whether there is a power in the TTOGRs to appoint a new trustee or to otherwise change the trustee; and

if, so, what the procedure or formalities are for doing so.

Changing trustee

relying on the Trustee Acts

If ability to change

trustee is not present, or is derelict, in the TTOGRs then the Trustee Acts in

states (and territories) provide options for appointing a new or additional

trustee which vary state to state.

Trustee Act – New South Wales

In New South Wales: section

6 of the Trustee Act (NSW) 1925

allows a person nominated for the purpose of appointing trustees in the TTOGRs,

a surviving trustee or a continuing trustee to appoint a new trustee in certain

specified situations such as where a trustee:

has died;

is incapable of acting as trustee; or

is absent for a specified period out of the state.

However an appointment of a new trustee in these situations must be effected by registered deed: sub-section 6(1) That is the deed of appointment must be registered with the general registry kept by the NSW Registrar-General, which is publicly searchable, and the applicable fee to so register the deed must be paid to NSW Land Registry Services for the appointment to take effect.

It is apparent from sub-section 6(13) that registration of a deed of appointment is not required where ability to appoint a new trustee is in the TTOGRs where the TTOGRs express a contrary intention; that is: where the TTOGRs expressly and effectively allow an appointment to be effected without a registered deed.

Trustee Act – Victoria

In Victoria there is a comparable capability for a person nominated for the purpose of appointing trustees in the TTOGRs, a surviving trustee or a continuing trustee to appoint a new trustee in writing in certain specified situations such as where a trustee:

has died;

is incapable of acting as trustee; or

is absent for a specified period out of the state;

under section 41 of the Trustee Act (Vic.) 1958. However this Victorian law does not impose any requirement that the required instrument of appointment in writing must be registered.

Changing trustee by obtaining a court order

The supreme courts of the states and territories are also given a residual statutory capability to appoint trustees under the respective Trustee Acts. However applying to a supreme court for an order to change a trustee of a FDT or a SMSF with sufficient supporting grounds is an option of last resort given likely significant costs and uncertainties of obtaining the order.

Changing trustee by deed

The TTOGRs in a trust deed of a FDT or a SMSF will frequently require that an appointment of a new trustee may or must be effected by a deed. It is desirable that it should do so to ensure the appointment of a new trustee does not become of a matter of uncertainty and difficulty for the reasons I have described in Redoing the deed.

Tax consequences of a change of trustee

As a change of trustee without more generally does not change beneficial

entitlements under a trust, the tax consequences are usually benign:

For capital gains tax (CGT), assurance that changing trustee does not give

rise to a CGT event for all of the CGT assets held in a trust is diffuse under

the Income Tax Assessment Act (C’th) (ITAA)

1997:

(2) You dispose of a * CGT asset if a change of ownership occurs from you to another entity, whether because of some act or event or by operation of law. However, a change of ownership does not occur if you stop being the legal owner of the asset but continue to be its beneficial owner.

Note: A change in the trustee of a trust does not constitute a change in the entity that is the trustee of the trust (see subsection 960-100(2)). This means that CGT event A1 will not happen merely because of a change in the trustee.

Sub-section 960-100(2) with the Notes below it in fact say:

(2) The trustee of a trust, of a superannuation fund or of an approved deposit fund is taken to be an entity consisting of the person who is the trustee, or the persons who are the trustees, at any given time.

Note 1: This is because a right or obligation cannot be conferred or imposed on an entity that is not a legal person.

Note 2: The entity that is the trustee of a trust or fund does not change merely because of a change in the person who is the trustee of the trust or fund, or persons who are the trustees of the trust or fund.

Similarly sections 104-55 and 104-60 of the ITAA 1997 which concern:

• Creating a trust over a CGT asset: CGT event E1

• Transferring a CGT asset to a trust: CGT event E2

each restate the above Note: viz.

Note: A change in the trustee of a trust does not constitute a change in the entity that is the trustee of the trust (see subsection 960-100(2)). This means that CGT event E… will not happen merely because of a change in the trustee.

Stamp duty

A change of trustee can have stamp duty consequences where the trust holds

dutiable property such as real estate.

Duty – NSW

Concessional stamp duty on the transfer of the dutiable property of the trust to the new trustee can be denied in NSW to a FDT unless the trust deed of the trust limits who can be a beneficiary, for anti-avoidance reasons: see sub-section 54(3) of the Duties Act (NSW) 1997.

Indeed Revenue NSW withholds the requisite satisfaction in sub-section 54(3) unless the TTOGRs provide or have been varied in such a way so that an appointed new trustee or a continuing trustee irrevocably cannot participate as a beneficiary of the trust. Contentiously satisfaction is withheld by Revenue NSW unless a variation to a FDT to so limit the beneficiaries is “irrevocable“ : see paragraph 6 of Revenue Ruling DUT 037, even though that variation may not be plausible or permissible under the TTOGRs of the FDT.

This hard line is taken by Revenue NSW to defeat schemes where someone, who might otherwise be a purchaser of dutiable property who would pay full duty on purchase of the property from the trust, becomes both a trustee and beneficiary able to control and beneficially own the property who is thus able to contrive liability only for concessional duty and avoid full duty,

Duty – Victoria

Although the Duties Act (Vic.) 2000 contains anti-avoidance provisions addressed at this kind of anti-avoidance arrangement, there is no comparable hard line to that in NSW in sub-section 33(3) of the Duties Act (Vic.) 2000 so that the transfer of dutiable property, including real estate, on changing trustee is more readily exempt from stamp duty.

Other requirements

A prominent requirement on changing trustee of a SMSF is notification to the Australian Taxation Office, as the regulator of SMSFs, within twenty-eight days of the change: see Changes to your SMSF at the ATO website.

Where changing trustee involves a corporate trustee then there may also be an obligation to inform the Australian Securities and Investments Commission of changes to details of directors of the corporate trustee, if any. There may be further matters to be addressed if any new or continuing directors are or will become non-residents of Australia and, with SMSFs, the general requirement in section 17A of the SIS Act that the parity between members of the fund on the one hand and trustees, or directors of the corporate trustee on the other, needs to borne in mind and, if need be, addressed.

Each of the state and territory duty jurisdictions include

declarations of trust over dutiable property (typically real estate) as

dutiable transactions in one form or another. Without a declaration of trust

head of duty, or an apt anti-avoidance provision, conveyancing duties that

would by paid on a transfer of the dutiable property to B can be avoided by A

declaring that property is held on trust for B though still held legally (on

title) by A. Duty on a declaration of trust generally applies at full rates

chargeable against the value of the dutiable property and differs from the head

of duty which applies to declarations of trust which are not made over dutiable

property to which a concessional duty or, in some states and territories, no duty will apply.

Duty eagerly assessed on the mention of a trust

So the Commissioners of State Revenues Australia wide are eager to assess any

document to duty which purports to contain a declaration of trust over dutiable

property which could be viewed

as either:

a

transfer of beneficial interest in the property in substance; or

a

disguised transfer.

Integrity of the state revenues

That zeal can be understood in the context of the integrity

of state revenues. In

New South Wales, where a “declaration of trust” is a dutiable transaction under

section 8 of the Duties Act 1997,

Revenue NSW will treat documents which foreshadow or even just mention a trust over dutiable property as

dutiable. Hence those who have an eye to the duty implications of deeds and

documents that impact dutiable property are justifiably cautious about using the expression “on trust” in a

deed or document where dutiable

conveyance of the beneficial ownership of dutiable property by that document is not intended.

Ambit declaration duty rejected

in W.A.

A recent case in Western Australia shows that duty on

documents that state that dutiable property is held on trust can be too readily

assessed as a declaration of

trust by state revenue. The W.A. Court of Appeal in In Rojoda Pty Ltd v. Commissioner of State

Revenue (WA) [2018] WASCA 224 decided against the Commissioner where two

deeds of dissolution of partnership in that case explicitly stated that a

partner, the surviving

registered owner of land, held dutiable property on

trust for other surviving partners of the partnerships. The Court of Appeal

found that the dissolution of two partnerships involving family members, whose

business included property ownership and investment, were not declarations of

trust and were not dutiable as declarations of trust over dutiable property.

It was determinative in Rojoda that the trusts recited in the deeds were confirmatory of trusts that already existed. It was significant that the Court of Appeal, in overturning a decision by the State Administrative Tribunal, was prepared to examine the equitable implications and the relevant legal and beneficial interests of the partners just before and on the execution of the deeds of dissolution of the partnerships. The Court of Appeal found that the legal and beneficial interests of the partners, just before the deeds were executed, were sufficiently comparable to the interests set out to be on trust in the deeds and thus held the deeds established no new trusts and thus did not declarations of trust in the context of the W.A. head of duty.

Identifiable new trust needed for a dutiable declaration of trust

The land had been used as partnership property of the partnerships. The Court of Appeal found that the wife, who was the surviving registered proprietor of the land, already held the land for the partners, which included the children of the wife and the husband, or their representatives. They thus had specific and fixed beneficial or equitable interests in the partnership properties before the deeds prepared for the dissolution of the partnerships were executed. These interests, reflecting their respective proportionate share of partnership property, were comparable interests to those said to be held on trust in the deeds. Thus the Court of Appeal found the trusts set out in the deeds were not new trusts declared over property dutiable in W.A.

The High Court has granted the Commissioner of State Revenue

special leave to appeal in Rojoda. This case will likely inform what amounts to a declaration of trust

dutiable in state and territory stamp jury jurisdictions.

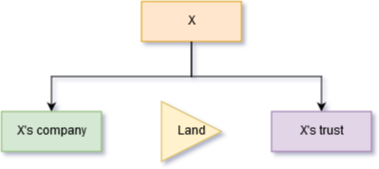

A company controlled by X owns land. X would prefer it if the land was held by a trust or in an individual name such as X or Y, X’s spouse.

Significant capital gains tax (“CGT”) on the transfer of the land is not expected by X and Y. Is a transfer of the land to a trust or to X or Y or both worthwhile? Here are some tax implications X may want to think about:

Capital gains tax

If the land has increased in value X will want to consider CGT more closely:

If the land is not an active asset, or if the small business CGT concessions or the new small business restructure roll-over, can’t apply for some other reason, the value of the land, when disposed of, will be taken into account in determining CGT. i.e. the market value substitution rule will apply in the event of an undervalue transfer of the land. An undervalue transfer of the land is rarely likely to be effective under tax rules.

The small business CGT concessions and the new small business restructure roll-over don’t apply if the asset is not an active asset. The land won’t be an active asset if it is mainly used by the company, and related parties of the company, to earn rent. As the land is held in a company, the 50% CGT discount is not available to the company on the transfer of the land.

Problems with a gift or an undervalue transfer

If full value is not payable to the company for the land then, without more, a transfer of the land could be treated as a dividend taxable in full to the transferee as a shareholder of the company, as a deemed dividend taxable to the transferee as an associate of the shareholders of the company, or may possibly be taxable to the company as a fringe benefit. Further if the company has taken the approach of gift there may be difficulties establishing that the company was legally entitled to give the land away to the transferee if that is what is done. Indications of a gift might give a creditor of the company additional rights to pursue the transferee for the value of the land that belonged to the company especially if the stance of the company is that the transfer was not any sort of dividend or remuneration to X or Y.

A sale of the land by the company for full value is more defensible. The sale can be on terms rather than for cash payable on settlement. If the transferee doesn’t follow through, and pay the value in cash or on the agreed terms, then the sale for value can be treated as a sham and the consequences of undervalue transfer can then follow.

So defensible transfers of the land include:

sales at full value on (genuine) terms; and

distribution of the value of the land to the shareholders of the company (not in the form of cash) on the voluntary liquidation of the company.

CGT event A1 – but watch out for CGT event E2 if a transfer to a trust

Usually CGT event A1 is attracted when land is transferred from one beneficial owner to another. CGT event A1 is taken to occur at the time of (in the income year of) the disposal, that is, the time of the transfer unless the transfer is made under a contract. If the transfer occurs under a contract and CGT event A1 applies, CGT event A1 is taken to occur at the time of making of the contract.

This can be significant where a contract and settlement straddle the end of an income year, with the time of the contract bringing forward the capital gain into the earlier income year if CGT event A1 applies. If the transferee is a related trust of the vendor then CGT event E2 can apply rather than CGT event A1. CGT event E2 though, unlike CGT event A1, does not bring forward the time of the CGT event to the time of the contract so, if CGT event E2 applies, the capital gain will be made in the later income year.

Stamp duty on a transfer

Stamp duty varies from state to state but generally applies to acquisitions of land based on the market value of the land, not the price to the transferee/purchaser. Very generally speaking it is usually charged at around 5% of the land value. The states offer limited stamp duty relief when acquisitions occur without a change in ultimate beneficial or economic ownership of the land. For instance, in New South Wales and Victoria relief exists in the form of corporate reconstruction concessions. These concessions are generally not available where the acquisition is by a trust or an individual. Thus stamp duty would need to be budgeted for by X as a further cost of transferring the land.

Goods and services tax

If the company is registered or ought to be registered for the goods and service tax and the land in used in an enterprise carried on by the company then the company may be obliged to charge 10% GST to the transferee on the transfer (taxable supply) of the land. If the transferee is also registered for GST, and will use the land in the transferee’s enterprise, then the transferee can obtain an input tax credit/refund of the GST charged to the transferee. The company and the transferee, if registered for GST, may also:

be able to claim the GST going concern exemption if they take the necessary steps for the exemption; or

be members of a GST group;

which would relieve the company of the obligation to charge GST to the transferee.

Hats off to Australian governments who have turned an imperative into a revenue opportunity. The Australian federal government regulator, the Foreign Investment Review Board (the FIRB), has not been well placed to track foreign purchases of real estate to date. The FIRB has been reliant on disclosure, and if prospective foreign buyers didn’t voluntarily disclose their planned land acquisitions, the FIRB has been none the wiser. There has been no register of (foreign) beneficial ownership of buyer entities which the FIRB can go and check even in the case of foreign real estate acquisitions completely prohibited under the foreign acquisitions law: the Foreign Acquisitions and Takeovers Act (C’th) 1975.

That has all changed. Buyers now need to demonstrate that they are not foreign to avoid hiked stamp duty in New South Wales, Victoria and Queensland. Foreigners who buy and sell Australian real estate are now under great scrutiny at both the buyer and seller ends of the land sale especially if the sale is for more than $750,000.

Big city real estate markets are buoyant, prices are high and foreign buyers are not exactly welcome by those looking to buy the same city real estate. The community has been surprised to learn that foreign purchases of Australian land have not been closely monitored. So, politically, it has been an opportune time to introduce these changes. Time will tell if they will be successful. They may well be. They will be a boon to the FIRB, but Australian buyers too will get caught up in the ramp up of imposts on foreign buyers. Why?

Buyers of Australian land

This is the bit for the FIRB. The New South Wales, Victorian and Queensland governments have just introduced hefty stamp duty and land tax surcharges on foreigners. From 21 June, 2016 a sworn Purchaser Declaration (“PD”) is now required from buyers, whether foreign or not, buying real estate in New South Wales. The PD is required along with stamp duty at the band the PD establishes that the buyer should pay to complete the conveyancing of a land sale. If the buyer of land in New South Wales is a foreign person (entity):

a 8% SURCHARGE (for the 2018 tax year, it was 4% for the 2017 tax year) on the stamp duty (i.e. extra) applies (it’s a 7% surcharge in Victoria);

the buyer is not entitled to the 12 month deferral for the payment of stamp duty for off-the-plan purchases of residential property; and

the buyer faces 2% SURCHARGE (for the 2018 tax year, it was 0.75% for the 2017 tax year) on land tax (i.e. extra).

It’s plain on the PD that the information is going to the ATO – it asks for the FIRB application number for the purchase. This will let the Australian Taxation Office (“ATO”) and the FIRB gather comprehensive data on foreign land acquisitions. Coupled with significantly increased penalties for breach of the foreign acquisitions rules, the availability of this information to the ATO and to the FIRB will give the federal government real capability to penalise unlawful real property acquisitions by foreigners.

Where an Australian buyer will be caught out too – example of a buyer that is an Australian-based family discretionary trust

It is notable that the PD doesn’t seek the confidential tax file number (understandable as the ATO can’t get the States to collect those) or the Australian Business Number (if any) of a buyer trust. It relies on the name of the buyer trust and a copy of the trust deed of the buyer trust with all amendments must be included with the PD.

If a foreign individual, company or trust is a potential beneficiary of the usual style of Australian family discretionary trust that is a New South Wales land buyer then, usually, the trustee can distribute 20% or more (Victoria – more than 50%) of the income and capital to that foreign person. That gives the foreign person a “significant interest” in the trust enough to cause the trust to be a foreign trust under these rules to whom the foreign stamp duty and land tax surcharges apply.

So if the copy trust deed supplied with the PD indicates that a remoter family member, who is not an Australian citizen or an Australian permanent resident, but is a foreigner who is a potential beneficiary of an (otherwise) Australian family discretionary trust ABLE to receive 20% of income or capital (more than 50% in Victoria), even if that remoter family member/foreigner may not have:

any current or past entitlement to income or capital of the trust; nor

any strong likelihood of participating in income or capital of the trust;

his or her eligibility under the trust deed exposes the trust to foreign trust/person status and liability for the stamp duty and land tax surcharges under these rules accordingly.

Sellers of Australian land

The ATO has had a problem collecting capital gains tax from sellers who are offshore after the sale of Australian land. Under tax treaties worldwide rights to tax interests in land are almost universally reserved to the governments where the land is. As other forms of assets and activity are moveable and relocatable taxation based on place is not so reserved because it is less effective than taxation based on residence and/or makes less sense.

So, frequently, when a non-resident sells land and makes a capital gain taxable in Australia, the ATO has no interaction with the non-resident, aside from due to their Australian landholding. This has often left the ATO with little leverage to assist them to collect tax debts arising from CGT on disposals of Australian land by non-residents ceasing investment in land in Australia.

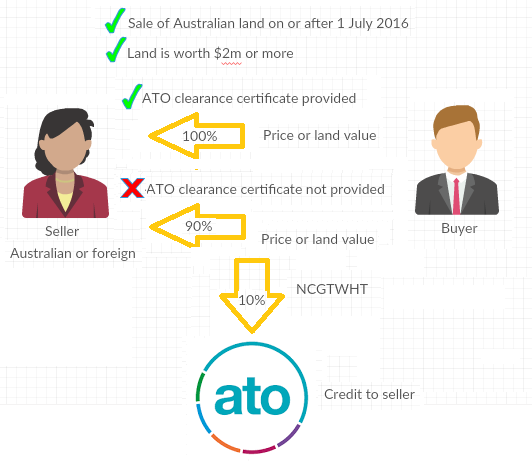

The solution is the tried and trusted withholding tax model. From 1 July, 2016, the non-resident capital gains tax withholding tax (“NCGTWHT”) is an obligation on the buyer (statistically likely to be a resident) to pay a non-final withholding tax to cover capital gains tax (likely to be) owing by the non-resident seller.

The NCGTWHT broadly applies as a non-final tax on sales of land worth more than $750,000 (from 1 July 2017, was $2m from 1 July 2016 to 30 June 2017). If the buyer does not receive an ATO clearance certificate from the seller then the buyer must withhold 12.5% (from 1 July 2017, was 10% from 1 July 2016 to 30 June 2017) of the value of the property (so 12.5% of the price for the land if it is an arms length sale, 12.5% of the “first element of the cost base” of the land to the acquirer if a CGT market value substitution rule applies in a non-arms length transaction).

Where an Australian seller will be caught out too – a non-final 12.5% tax

It is of no consequence that the seller is, or might be, an Australian resident/tax resident and the buyer is assured of this. There is no “reason to believe the seller is an Australian resident” exception for sales of freehold interests in land. Even the seller could be wrong – tax residence can a vexed question which is frequently litigated in tax cases.

The liability to the ATO is on the buyer unless the seller can obtain and provide a clearance certificate from the ATO to the buyer no later than settlement of the land sale so, if the seller does not return and pay the CGT on the seller for the sale, the NCGTWHT paid by the buyer on the seller’s behalf won’t be refunded.

Template contracts for the sale of land across Australia have been hastily adjusted to include conditions confirming that, where the land is worth more than $750,000:

the buyer can contractually withhold the NCGTWHT from the price if the clearance certificate is not provided; and

the seller can be assured that the NCGTWHT will be paid immediately by the buyer to the ATO to the credit of the seller.