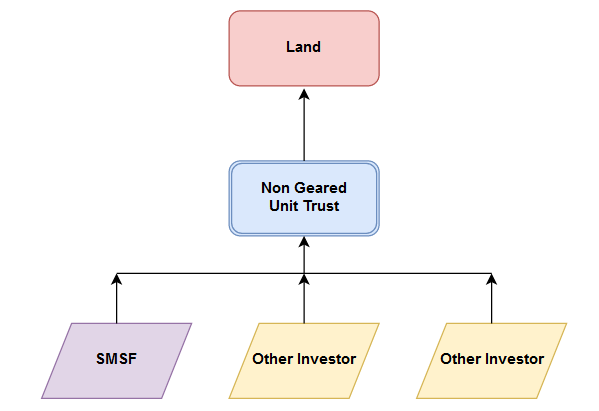

A popular pro-active SMSF strategy is to skirt the boundaries of the associate rules in Part 8 of the Superannuation Industry (Supervision) Act 1993 (SISA) with minority SMSF investors taking units in a unit trust with no apparent majority controller with other unrelated SMSF or non-SMSF investors. The object of the minority strategy is that the minority SMSF investor and associates have a less than 50% entitlement to income and capital of the unit trust and so the unit trust will not be a related trust of the SMSF automatically. This is an alternative strategy to investing in a non-geared unit trust which complies with Regulation 13.22C of the Superannuation Industry (Supervision) Regulations.

A popular pro-active SMSF strategy is to skirt the boundaries of the associate rules in Part 8 of the Superannuation Industry (Supervision) Act 1993 (SISA) with minority SMSF investors taking units in a unit trust with no apparent majority controller with other unrelated SMSF or non-SMSF investors. The object of the minority strategy is that the minority SMSF investor and associates have a less than 50% entitlement to income and capital of the unit trust and so the unit trust will not be a related trust of the SMSF automatically. This is an alternative strategy to investing in a non-geared unit trust which complies with Regulation 13.22C of the Superannuation Industry (Supervision) Regulations.

If the minority strategy doesn’t work

If the unit trust is, or becomes, a related trust of the SMSF the consequences can be severe. The investment in the related trust by the SMSF is taken to be an in-house asset. A SMSF that fails to remedy an investment of more than 5% of its assets in in-house assets faces loss of complying status potentially causing:

- tax at 47% on its current income; and

- loss of almost half of the assets of the SMSF in a one-off additional tax bill in the year in which the SMSF becomes non-complying; or

- prosecution for civil or criminal breach of a civil penalty provision under the SISA.

An investment in a non-geared unit trust which complies with Regulation 13.22C is specifically excluded from being an in-house asset. The minority strategy does not give the same assurance to a SMSF investor in units in a unit trust which is not Regulation 13.22C compliant.

Control of a trust

The more than 50% entitlement to income and capital test is one of the tests of control of a trust in sub-section 70E(2) of the SISA which determine whether or not a trust is controlled and is thus an associate and, by that, a related trust. An alternate test in paragraph 70E(2)(b), sometimes overlooked by users of the minority strategy, is the directions, instructions or wishes test which is an alternative test of control of a trust. Its formulation:

an entity controls a trust if:

… (b) the trustee of the trust, or a majority of the trustees of the trust, is accustomed or under an obligation (whether formal or informal), or might reasonably be expected, to act in accordance with the directions, instructions or wishes of a group in relation to the entity (whether those directions, instructions or wishes are, or might reasonably be expected to be, communicated directly or through interposed companies, partnerships or trusts);

is based on a similar formulation in sub-section 318(6) of the Income Tax Assessment Act 1936 which deals with associates under the income tax controlled foreign corporations (CFC) rules.

MWYS v. Commissioner of Taxation

The directions, instructions or wishes test in paragraph 318(6)(b) in the CFC rules was recently considered by the Administrative Appeals Tribunal in MWYS v. Commissioner of Taxation [2017] AATA 3037 (22 December 2017) and the companies in dispute with the Commissioner in that case were found not to be associated even though the companies concerned had the same directors.

Deputy President Logan found that, despite the unanimity of the directors of the companies involved, the companies were not associates as it could not be concluded, on the evidence, that the directors of one company, acting in that capacity, would influence themselves acting in their capacity as directors of the other company. Deputy President Logan observed that the arrangements between the companies involved: an Australian listed company and a UK publicly listed company which enabled them to dual list on the ASX and the London Stock Exchange, were for the purpose of compliance with dual listing requirements but, within that framework, the companies were structured with similarity to unrelated joint venturers. No inference could be drawn about one company acting on the directions of the other.

Moreover the strict governance which applied to both of the listed companies actually helped the companies to establish that the directors were acting independently and at arms length from the other company even where the directors were directors of the other company too. Short of a sham, or a cipher, as arose in Bywater Investments Ltd v Federal Commissioner of Taxation [2016] HCA 45 (see our blog -Why setting up offshore companies for Australians is a tricky business), the AAT was prepared to rely on the meticulous corporate documents which set out the distinct responsibilities of the directors of the companies they separately served.

Directors in common

It is certainly clear from MWYS that commonality of directors of a company, or in the case of paragraph 70E(2)(b) of the SISA, commonality of directors of a corporate trustee is not enough, in itself, to amount to a reasonable expectation that one company will act in accordance with the directions, instructions or wishes of the other company or of a group including it.

Is MWYS good news for SMSFs using the minority strategy?

Is the decision in MWYS a relief to minority SMSF investors in unit trusts concerned about paragraph 70E(2)(b) of the SISA? Maybe not. Documents of SMSF trustees and of unit trusts, in which they invest, are far less likely to be as meticulous at keeping the affairs of entities being examined for control apart. A unit trust deed is more likely than, say, a joint venture arrangement to show that the trustee of a unit trust might act in accordance with the directions, instructions or wishes of a unitholder, albeit a minority unitholder.

Frequently, under unit trust deeds, minority unitholders have the right to vote on resolutions which bind the trustee of the unit trust to act. A minority unitholder may not have the votes, alone, to so bind the trustee; but the question posed by the test is whether the trustee is accustomed to act, or whether there is a reasonable expectation that the trustee of the unit trust will act, in accordance with the directions, instructions or wishes of a minority unitholder. The answer in fact is equivocal – yes, if the minority unitholder votes are in the majority and no, if not. So yes, a part of the time or on some occasions. So the minority SMSF investor and the trustee of the unit trust are associated?

What will facts show under scrutiny?

The concern for SMSF users of the minority strategy is: will their position, that the unit trust they invest in is not a related trust, become less defensible under scrutiny from the Commissioner? From the activities of the SMSF investor, its associates and the trustee of the unit trust the Commissioner can gauge how the trustee of the unit trust has reached decisions, which may not have been in accord with documents, whether sound or not, and form a view as to how likely the trustee of the unit trust is likely to have acted on directions, instructions or wishes of the SMSF investor and its associates.

Until the circumstances of a SMSF using a minority strategy, including the relevant documents, are considered it can be uncertain whether a SMSF minority unitholder may “control” a unit trust and cause it to be a related trust.